NCBJ Panel Discusses New Consumer Loan Products

11/05/19

One of the best panels that I attended at NCBJ was New Consumer Loan Products and Potential Bankruptcy Issues The panel included Tyler Brown from Hunton Andrews Kurth, Carol Evans from the Federal Reserve Bank of Washington, D.C., Prof. Adam Levitin from Georgetown University Law Center and Gary Reeder, Vice-President of Innovation and Policy at the Center for Financial Innovation.

What Is Fintech?

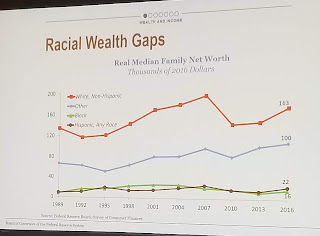

Carol Evans from the Federal Reserve discussed the recent survey of household economics and decisionmaking. 12% could not cover unexpected $400 expense while 27% would have to borrow or sell assets to do so. Meanwhile, the racial wealth gap is widening. These developments create both a need for new consumer loan products and a risk that consumers will be victimized by them.

Fintechs are an important player in the consumer market. Fintechs are the companies in this space while fintech is the product they offer. Fintech spans a continuum ranging from the ATM to innovative credit scoring to transferring money by mobile phones. Fintechs do not have not a brick and mortar presence. Instead, they interact with consumers online through the web or an app

Fintech has a lower cost of underwriting which can improve financial inclusion. Some Fintech companies also provide consumers with budgeting assistance. Additionally, 32% of small businesses used online lenders in 2018.

Early Wage Access is an employee benefit being offered by some employers. It is a variation of payday lending.

Alternative Data

Another trend in Fintech is the use of alternative data, which is data outside of a credit report. Some data sources don’t have an obvious connection to lending and may be proxies for race, gender, etc. Facebook friends and social networks are one example. If your Facebook friends have a poor credit history, you may have poor credit as well. However, cash flow underwriting, which looks at the funds flowing through your bank account can help if you have gig economy income.

Targeted marketing poses a risk of discrimination. For example, Asian Americans might be charged more for test preparation products. Consumers might be might be offered different products based on race, gender, national origin. HUD has sued Facebook because advertisers on Facebook could target ads based on prohibited categories. HUD alleged that Facebook was facilitating redlining.

The fact that an algorithm is data driven does not ensure that it is fair or objective. Amazon developed an algorithm for hiring technical positions. It turned out that it would have discriminated against women and was never implemented.

Issues With Student Loans

Both Gary Reeder and Prof. Levitin discussed issues related to student loans. Financial institutions that don’t just provide student loans are offering to refinance student loan debt. Examples are Future Fuel, Six Up and Vemo. How do you determined dischargeability when student loans and consumer loan combined. Once you pierce that layer of protection, the entire pool is polluted. However, if you solely consolidate student loans it’s ok. What if administrative costs are rolled in. Is that still solely a non-dischargeable student loan?

The recent Crocker opinion from the Fifth Circuit shows that not all private loans fit the definition of a nondischargeable student loan. In Crocker, a loan to study for the bar exam was found to be dischargeable. Merely saying something is a student loan may not be enough to keep it from being dischargeable.

There has been a trend in for profit colleges failing. The Department of Education is supposed to have a program to forgive student loans from for profits that fail. However, this is made more difficult by the fact that there may be multiple counterparties

Prof. Levitin spoke about income sharing agreements. Income sharing agreements are alternate forms of student loan financing. Instead of borrowing a sum certain, a student agrees to pay a fixed percentage of income for a fixed period of years over a fixed minimum. A student with a high wage job pays more than someone with a minimum wage job. It is like an Income Contingent Repayment Plan on the front end. They are not widespread. Purdue University and some nonaccredited institutions are offering financing through ISAs. ISAs are not a good financing mechanism compared to traditional federal student loans. They compete with private student loans.

Are ISAs credit? If they constitute credit, it implicates many federal statutes. What if the plan offered is different for computer science majors v. African American studies majors?

In bankruptcy, is an ISA a claim? Is it dischargeable? Accrued but unpaid obligations are clearly claims. Future obligations are probably also a claim, but there is a little more room to argue. Is it secured? Is it perfected? How do you deal with it in a chapter 13?

Choice of Law

Choice of law is becoming a hot topic. Online installment lending has increased to $50 billion outstanding. Lenders have an incentive to shop for state law which is beneficial to them. Prof. Levitin gave the example of a lender in Utah with borrowers in 30 states. The contract designates Utah law.

The first question is regulatory. Can a state regulate an out of state lender offering credit to its citizens? The Tenth Circuit said that Kansas can require regulation of a non-Kansas lender. The Seventh Circuit reached an opposite result, but the facts were unusual. An Illinois lender was making loans to Indiana borrowers, but the borrowers had to physically go to Illinois.

In choice of law analysis, the first question is does the contractual choice of law have a rational relationship to the transaction. If there is only a nominal relationship, then maybe not. The second question is whether the choice of law is offensive to the law of the borrower's state.

There have been some creative choice of law provisions used by online lenders, such as Maltese law or Cook island law. The panel did not have a lot of confidence that this would work for purely online lenders. Another angle is partnerships between online lenders and banks or Native American tribes. Rent a bank is a scheme where a bank originates a loan and then assigns it to a nonbank lender. Is federal preemption assignable? This is hotly debatable. One bankruptcy court has held that a loan is enforceable if it was valid when made. There arrangements are vulnerable to two lines of attack. First, there is the argument under the Madden Doctrine that federal preemption is not assignable. The law should look at the characteristics of the current lender, not the loan. Even if there might be assignability, parties can bring up the true lender doctrine. Who did marketing? Who has the credit risk? Who does the servicing? However, it may not even be necessary to assign the loan. If the originating bank issues a participation or a credit default swap, the loan stays on the bank’s books. Prof. Levitin argued that courts need to require certification that the economic interest has not been transferred. According to Mr. Reeder, the next twist is to assign, then securitize. A securitization trust sponsored by a bank is not itself a bank.

Merchant Cash Advances

[more]

Mr. Reeder talked about Merchant Cash Advances. These are similar to wage advances but for small businesses. Money transferred from an entity to a recipient. The person who receives the advance has a contractual obligation to pay a percentage of its future revenue up to ceiling. So what is the nature of relationship. The MCA company provided cash and it will be provided cash plus a return in the future. Is it a debt? There are three core reasons for arguing that it is not a debt. First, the MCA party can avoid licensing requirements. Next is the disclosure regime. If it's not a debt, then Truth in Lending disclosures don’t apply. Finally usury caps don’t apply if it is not a loan.

In bankruptcy, when an MCA party shows up and says it has a "claim," does it? It is the problem of calling something an advance not a loan. States are looking at these transactions. If it is not a loan, does it ride through the bankruptcy unaffected? When someone guarantees an MCA, what are they guaranteeing? Are they guaranteeing payment of the MCA obligation or merely performance by the obligor and is there a difference?

My partner, Barbara Barron, and I recently authored an article on MCAs called "Why MCA? Adding Havoc to Chaos" which appears in Vol. 33, Issue 3 of Commercial Law World. I would be happy to provide a copy to anyone who requests it by sending an email to [email protected].

- Feeds Categories: