HAMP: "You Probably Think This LAW Is About YOU!"

11/15/10

[more]

[more]

This posting's title, with apologies to Carly Simon who wrote and sung Billboard's 72nd most popular song ever, is appropriate if any of us think that the Mortgage Modification issues and Programs, like HAMP, are about us; they are all about the Servicers/Lenders and the INVESTORS of the ubiquitous Mortgage-Backed Securities ("MBS").

This posting's title, with apologies to Carly Simon who wrote and sung Billboard's 72nd most popular song ever, is appropriate if any of us think that the Mortgage Modification issues and Programs, like HAMP, are about us; they are all about the Servicers/Lenders and the INVESTORS of the ubiquitous Mortgage-Backed Securities ("MBS").

The program, which has no teeth for enforcement by any entity (Treasury, FDIC, Federal Reserve, etc.) was established to protect the INVESTMENT pools of securitized mortgages. This means simply that the mortgage and investment communities refused to permit any government force-down of a program that might hurt "ROI" or "Return on Investment", or more crudely put, the PROFITS and INCOME made by the owners of these mortgage pools, and by the Goldman Sachs and Lehman Brothers of the world - the people who brought us the "great meltdown"

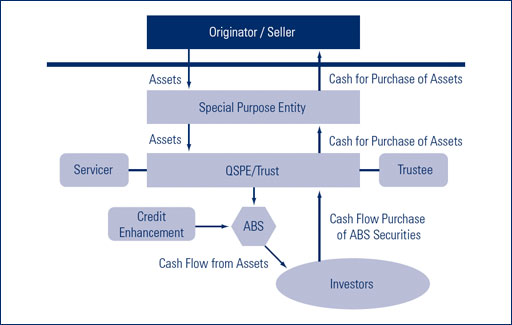

In fairness, the whole idea behind putting a large number of mortgages together, computing the average interest rate to be paid by homeowners, while at the same time calculating the expected or historical number of "bad" (non-paying) loans, was to enlarge the market of home ownership. By putting the mortgages into securities, all of the mortgage originators, brokers, lenders, banks, mortgage companies, who made these mortgage loans were "off the hook".

As stated in earlier posts, only the investors had anything to lose and they had done their homework. They figured out how much to pay for $1 billion of what became a BOND secured by home mortgages. What could be safer? Based on past experience, the Depression aside, the answer was Nothing Could Be Safer! Or maybe not!!!

During the early musings about what to do as the market was plummeting, and Mortgage-Backed Securities were being valued at $0 - high figures of 40% of face value, there were many theories put forth as to "What Do We Do Now?". One of those concepts was to have Congress and the Supreme Court declare that the contract making up these pools of mortgages, could be broken, for the sake of national security. Remember, our financial stability was gone and the markets were in free-fall.

Rejecting that idea, and rather than one of the Federal Government's arms publicly insuring that no MBS would drop below 70% of face value because the Federal Government would guaranty the FIRST 30% of losses which would have stopped the spiral down, the free-market system functioned as it is designed to do, and we ended up with the mess we are in currently regarding FORECLOSURES!!

The Making Home Affordable ("MHA") program which gave birth to "HAMP" really was a deal with the mortgage and securities industries. The program is about making sure that profits stay high enough to continue to attract buyers of MBS. The way to accomplish that goal is to NOT make modifications that will hurt the INVESTOR - Homeowners be damned. 9%-10% unemployment is no excuse for defaulting on your mortgage payment. If you can catch up fast enough you get to keep your house. If not, well, the house goes to sale at auction -but you can't bid -HA! Gotcha!

Realize that the reason the rules do not help most of the homeowners applying for modifications, or foolishly, a principal write-down, is that they are not supposed to. The rules are there, as written, to protect investors. Well, YES and NO!. If the investors take significant losses, the spiral down starts again and soon a family homestead will consist of two large tents.

Author's Copyright by Richard I. Isacoff, Esq